/

Автор: Hull J.C.

Теги: finance economics financial capital stock market

ISBN: 0- 13-009056-5

Год: 2002

Текст

г

Options, Futures,

AND

Other Derivatives

FIFTH EDITION

JOHN C. Hull’s Options, Futures, and Other Derivatives is unique in that it is both

a best-selling college textbook and the “bible” in trading rooms throughout the world.

The Fifth Edition continues to offer the most current topics in the field with the addition

of seven NEW chapters:

Chapter 4 “Hedging Strategies Using Futures,” a new chapter on the use of futures for hedging.

Chapter 20 “More on Models and Numerical Procedures.”

Chapter 25 “Swaps Revisited,” gives the reader insight into the range of nonstandard swap products.

Chapter 27 “Credit Derivatives,” explains how these products work and how they should be valued.

Chapter 28 “Real Options,” provides realistic examples showing how the real options approach can be used in capital investment appraisal.

Chapter 29 “Insurance, Weather, and Energy Derivatives,” explains non-traditional derivatives and their role in risk management.

Chapter 30 “Derivatives? Mishaps, and What We Can Learn From Them.”

A new version of DerivaGem Software (Version 1.50) comes with every copy of the text. It includes a

new Applications Builder module. Updates to the software can be downloaded from

www.prenhall.com/lnill.

Pearson

Education

Prentice Hall

Upper Saddle River, New Jersey 07458

www.prenhall.coin

PRENTICE HALL FINANCE SERIES

Personal Finance

Keown, Personal Finance: Turning Money into Wealth, Second Edition

Trivoli, Personal Portfolio Management: Fundamentals d Strategies

Winger/Frasca, Personal Finance: An Integrated Planning Approach. Sixth Edition

Undergraduate Investments/Portfolio Management

Alexander/Sharpe/Bailey. Fundamentals of Investments, Third Edition

Fabozzi. Investment Management, Second Edition

Haugen, Modern Investment Theory, Fifth Edition

Haugen. The Neu- Finance, Second Edition

Haugen. The Beast on Wall Street

Haugen. The Inefficient Stock Market. Second Edition

Holden, Spreadsheet Modeling: A Book and CD-ROM Series

(Available in Graduate and Undergraduate Versions)

Nofsinger. The Psychology of Investing

Taggart, Quantitative Analysis for Investment Management

Winger/Frasca, Investments, Third Edition

Graduate Investments/Portfolio Management

Fischer/Jordan. Security Analysis and Portfolio Management, Sixth Edition

Francis/Ibbotson. Investments: A Global Perspective

Haugen. The Inefficient Stock Market, Second Edition

Holden, Spreadsheet Modeling: A Book and CD-ROM Series

(Available in Graduate and Undergraduate Versions)

Nofsinger, The Psychology of Investing

Sharpe,Alexander/Bailey. Investments, Sixth Edition

Options/Futures/Derivatives

Hull, Fundamentals of Futures and Options Markets. Fourth Edition

Hull, Options, Futures, and Other Derivatives, Fifth Edition

Risk Management/Financial Engineering

Mason/Merton,Perold/Tufano, Cases in Financial Engineering

Fixed Income Securities

Handa, FinCoach: Fixed Income (software)

Bond Markets

Fabozzi, Bond Markets, Analysis and Strategics, Fourth Edition

Undergraduate Corporate Finance

Bodie/Merton, Finance

Emery/Finnerty Stowe. Principles of Financial Management

Emery/Finnerty. Corporate Financial Management

Gallagher/Andrew. Financial Management: Principles and Practices, Third Edition

Handa, FinCoach 2.0

Holden, Spreadsheet Modeling: A Book and CD-ROM Series

(Available in Graduate and Undergraduate Versions)

Keown/Martin/Petty'Scott. Financial Management, Ninth Edition

Keown/Martin/Petty/Scott, Financial Management, 9/e activebook™

Keown/Martin/Petty/Scott. Foundations of Finance: The Logic and Practice of Financial Management, Third Edition

Keown;Martin,'Petty/Scott, Foundations of Finance, activebook™

Mathis, Corporate Finance Live: A Web-based Math Tutorial

Shapiro'Balbirer, Modern Corporate Finance: A Multidisciplinary Approach to Value Creation

Van Horne/Wachowicz, Fundamentals of Financial Management, Eleventh Edition

Mastering Finance CD-ROM

Fifth Edition

OPTIONS, FUTURES,

& OTHER DERIVATIVES

John C. Hull

Maple Financial Group Professor of Derivatives and Risk Management

Director, Bonham Center for Finance

Joseph L. Rotman School of Management

University of Toronto

Prentice

Hall

PRENTICE HALL, UPPER SADDLE RIVER, NEW JERSEY 07458

CONTENTS

Preface....................................................................................xix

1. Introduction..............................................................................1

1.1 Exchange-traded markets.......................................................1

1.2 Over-the-counter markets......................................................2

1.3 Forward contracts.............................................................2

1.4 Futures contracts.............................................................5

1.5 Options.......................................................................6

1.6 Types of traders.............................................................10

1.7 Other derivatives............................................................14

Summary......................................................................15

Questions and problems.......................................................16

Assignment questions.........................................................17

2. Mechanics of futures markets.............................................................19

2.1 Trading futures contracts....................................................19

2.2 Specification of the futures contract........................................20

2.3 Convergence of futures price to spot price...................................23

2.4 Operation of margins.........................................................24

2.5 Newspaper quotes.............................................................27

2.6 Keynes and Hicks.............................................................31

2.7 Delivery.....................................................................31

2.8 Types of traders.............................................................32

2.9 Regulation...................................................................33

2.10 Accounting and tax...........................................................35

2.11 Forward contracts vs. futures contracts......................................36

Summary......................................................................37

Suggestions for further reading..............................................38

Questions and problems.......................................................38

Assignment questions.........................................................40

3. Determination of forward and futures prices.............................................41

3.1 Investment assets vs. consumption assets.....................................41

3.2 Short selling................................................................41

3.3 Measuring interest rates.....................................................42

3.4 Assumptions and notation.....................................................44

3.5 Forward price for an investment asset........................................45

3.6 Known income.................................................................47

3.7 Known yield..................................................................49

3.8 Valuing forward contracts....................................................49

3.9 Are forward prices and futures prices equal?.................................51

3.10 Stock index futures..........................................................52

3.11 Forward and futures contracts on currencies..................................55

3.12 Futures on commodities.......................................................58

ix

X

Contents

3.13 Cost of carry..............................................................60

3.14 Delivery options...........................................................60

3.15 Futures prices and the expected future spot price..........................61

Summary....................................................................63

Suggestions for further reading............................................64

Questions and problems.....................................................65

Assignment questions.......................................................67

Appendix ЗА: Proof that forward and futures prices are equal when interest

rates are constant..........................................................68

4. Hedging strategies using futures.......................................................70

4.1 Basic principles...........................................................70

4.2 Arguments for and against hedging..........................................72

4.3 Basis risk.................................................................75

4.4 Minimum variance hedge ratio...............................................78

4.5 Stock index futures........................................................82

4.6 Rolling the hedge forward..................................................86

Summary....................................................................87

Suggestions for further reading............................................88

Questions and problems.....................................................88

Assignment questions.......................................................90

Appendix 4A: Proof of the minimum variance hedge ratio formula.............92

5. Interest rate markets.............................................................93

5.1 Types of rates.............................................................93

5.2 Zero rates.................................................................94

5.3 Bond pricing...............................................................94

5.4 Determining zero rates.....................................................96

5.5 Forward rates..............................................................98

5.6 Forward rate agreements...................................................100

5.7 Theories of the term structure............................................102

5.8 Day count conventions.....................................................102

5.9 Quotations................................................................103

5.10 Treasury bond futures......................................................104

5.11 Eurodollar futures.........................................................110

5.12 The LIBOR zero curve.......................................................Ill

5.13 Duration...................................................................112

5.14 Duration-based hedging strategies..........................................116

Summary...................................................................118

Suggestions for further reading...........................................119

Questions and problems....................................................120

Assignment questions......................................................123

6. Swaps.................................................................................125

6.1 Mechanics of interest rate swaps..........................................125

6.2 The comparative-advantage argument........................................131

6.3 Swap quotes and LIBOR zero rates..........................................134

6.4 Valuation of interest rate swaps..........................................136

6.5 Currency swaps............................................................140

6.6 Valuation of currency swaps...............................................143

6.7 Credit risk...............................................................145

Summary...................................................................146

Suggestions for further reading...........................................147

Questions and problems....................................................147

Assignment questions......................................................149

Contents

xi

7. Mechanics of options markets...........................................................151

7.1 Underlying assets...........................................................151

7.2 Specification of stock options..............................................152

7.3 Newspaper quotes............................................................155

7.4 Trading.....................................................................157

7.5 Commissions.................................................................157

7.6 Margins.....................................................................158

7.7 The options clearing corporation............................................160

7.8 Regulation..................................................................161

7.9 Taxation....................................................................161

7.10 Warrants, executive stock options, and convertibles.........................162

7.11 Over-the-counter markets....................................................163

Summary....................................................................163

Suggestions for further reading............................................164

Questions and problems.....................................................164

Assignment questions.......................................................165

8. Properties of stock options............................................................167

8.1 Factors affecting option prices.............................................167

8.2 Assumptions and notation....................................................170

8.3 Upper and lower bounds for option prices....................................171

8.4 Put-call parity.............................................................174

8.5 Early exercise: calls on a non-dividend-paying stock........................175

8.6 Early exercise: puts on a non-dividend-paying stock.........................177

8.7 Effect of dividends.........................................................178

8.8 Empirical research..........................................................179

Summary....................................................................180

Suggestions for further reading............................................181

Questions and problems.....................................................182

Assignment questions.......................................................183

9. Trading strategies involving options...................................................185

9.1 Strategies-involving a single option and a stock............................185

9.2 Spreads.....................................................................187

9.3 Combinations................................................................194

9.4 Other payoffs...............................................................197

Summary....................................................................197

Suggestions for further reading............................................198

Questions and problems.....................................................198

Assignment questions.......................................................199

10. Introduction to binomial trees........................................................200

10.1 A one-step binomial model...................................................200

10.2 Risk-neutral valuation......................................................203

10.3 Two-step binomial trees.....................................................205

10.4 A put example...............................................................208

10.5 American options............................................................209

10.6 Delta.......................................................................210

10.7 Matching volatility with и and d............................................211

10.8 Binomial trees in practice..................................................212

Summary....................................................................213

Suggestions for further reading............................................214

Questions and problems.....................................................214

Assignment questions.......................................................215

xii

Contents

11. A model of the behavior of stock prices.................................................216

11.1 The Markov property..........................................................216

11.2 Continuous-time stochastic processes.........................................217

11.3 The process for stock prices.................................................222

11.4 Review of the model..........................................................223

11.5 The parameters...............................................................225

11.6 Ito’s lemma..................................................................226

11.7 The lognormal property.......................................................227

Summary......................................................................228

Suggestions for further reading..............................................229

Questions and problems.......................................................229

Assignment questions.........................................................230

Appendix HA: Derivation of Ito’s lemma.......................................232

12. The Black-Scholes model.................................................................234

12.1 Lognormal property of stock prices...........................................234

12.2 The distribution of the rate of return.......................................236

12.3 The expected return..........................................................237

12.4 Volatility...................................................................238

12.5 Concepts underlying the Black-Scholes-Merton differential equation...........241

12.6 Derivation of the Black-Scholes-Merton differential equation.................242

12.7 Risk-neutral valuation.......................................................244

12.8 Black-Scholes pricing formulas...............................................246

12.9 Cumulative normal distribution function......................................248

12.10 Warrants issued by a company on its own stock.................................249

12.11 Implied volatilities.........................................................250

12.12 The causes of volatility.....................................................251

12.13 Dividends....................................................................252

Summary......................................................................256

Suggestions for further reading..............................................257

Questions and problems.......................................................258

Assignment questions.........................................................261

Appendix 12A: Proof of Black-Scholes-Merton formula.........................262

Appendix 12B: Exact procedure for calculating the values of American calls on

dividend-paying stocks......................................................265

Appendix 12C: Calculation of cumulative probability in bivariate normal

distribution................................................................266

13. Options on stock indices, currencies, and futures.......................................267

13.1 Results for a stock paying a known dividend yield............................267

13.2 Option pricing formulas......................................................268

13.3 Options on stock indices.....................................................270

13.4 Currency options.............................................................276

13.5 Futures options..............................................................278

13.6 Valuation of futures options using binomial trees ...........................284

13.7 Futures price analogy........................................................286

13.8 Black’s model for valuing futures options....................................287

13.9 Futures options vs. spot options.............................................288

Summary......................................................................289

Suggestions for further reading..............................................290

Questions and problems.......................................................291

Assignment questions.........................................................294

Appendix 13A: Derivation of differential equation satisfied by a derivative

dependent on a stock providing a dividend yield....................295

Contents

xiii

Appendix 13B: Derivation of differential equation satisfied by a derivative

dependent on a futures price.......................................297

14. The Greek letters........................................................................299

14.1 Illustration..................................................................299

14.2 Naked and covered positions...................................................300

14.3 A stop-loss strategy..........................................................300

14.4 Delta hedging.................................................................302

14.5 Theta.........................................................................309

14.6 Gamma.........................................................................312

14.7 Relationship between delta, theta, and gamma..................................315

14.8 Vega..........................................................................316

14.9 Rho...........................................................................318

14.10 Hedging in practice...........................................................319

14.11 Scenario analysis.............................................................319

14.12 Portfolio insurance...........................................................320

14.13 Stock market volatility.......................................................323

Summary.......................................................................323

Suggestions for further reading...............................................324

Questions and problems............"...........................................326

Assignment questions..........................................................327

Appendix 14A: Taylor series expansions and hedge parameters...................329

15. Volatility smiles........................................................................330

15.1 Put-call parity revisited.....................................................330

15.2 Foreign currency options......................................................331

15.3 Equity options................................................................334

15.4 The volatility term structure and volatility surfaces.........................336

15.5 Greek letters.................................................................337

15.6 When a single large jump is anticipated...............................338

15.7 Empirical research............................................................339

Summary.......................................................................341

Suggestions for further reading...............................................341

Questions and problems........................................................343

Assignment questions..........................................................344

Appendix 15A: Determining implied risk-neutral distributions from volatility

smiles........................................................................345

16. Value at risk............................................................................346

16.1 The VaR measure...............................................................346

16.2 Historical simulation.........................................................348

16.3 Model-building approach.......................................................350

16.4 Linear model..................................................................352

16.5 Quadratic model...............................................................356

16.6 Monte Carlo simulation........................................................359

16.7 Comparison of approaches......................................................359

16.8 Stress testing and back testing...............................................360

16.9 Principal components analysis.................................................360

Summary.......................................................................364

Suggestions for further reading...............................................364

Questions and problems........................................................365

Assignment questions..........................................................366

Appendix 16A: Cash-flow mapping...............................................368

Appendix 16B: Use of the Cornish-Fisher expansion to estimate VaR.............370

xiv

Contents

17. Estimating volatilities and correlations...............................................372

17.1 Estimating volatility........................................................372

17.2 The exponentially weighted moving average model..............................374

17.3 The GARCH(1,1) model.........................................................376

17.4 Choosing between the models..................................................377

17.5 Maximum likelihood methods...................................................378

17.6 Using GARCH(1, 1) to forecast future volatility..............................382

17.7 Correlations.................................................................385

Summary.....................................................................388

Suggestions for further reading.............................................388

Questions and problems......................................................389

Assignment questions........................................................391

18. Numerical procedures...................................................................392

18.1 Binomial trees...............................................................392

18.2 Using the binomial tree for options on indices, currencies, and futures

contracts..........................................................................399

18.3 Binomial model for a dividend-paying stock...................................402

18.4 Extensions to the basic tree approach........................................405

18.5 Alternative procedures for constructing trees................................406

18.6 Monte Carlo simulation.......................................................410

18.7 Variance reduction procedures................................................414

18.8 Finite difference methods....................................................418

18.9 Analytic approximation to American option prices.............................427

Summary.....................................................................427

Suggestions for further reading.............................................428

Questions and problems......................................................430

Assignment questions........................................................432

Appendix 18A: Analytic approximation to American option prices of

MacMillan and of Barone-Adesi and Whaley.....................................433

19. Exotic options.........................................................................435

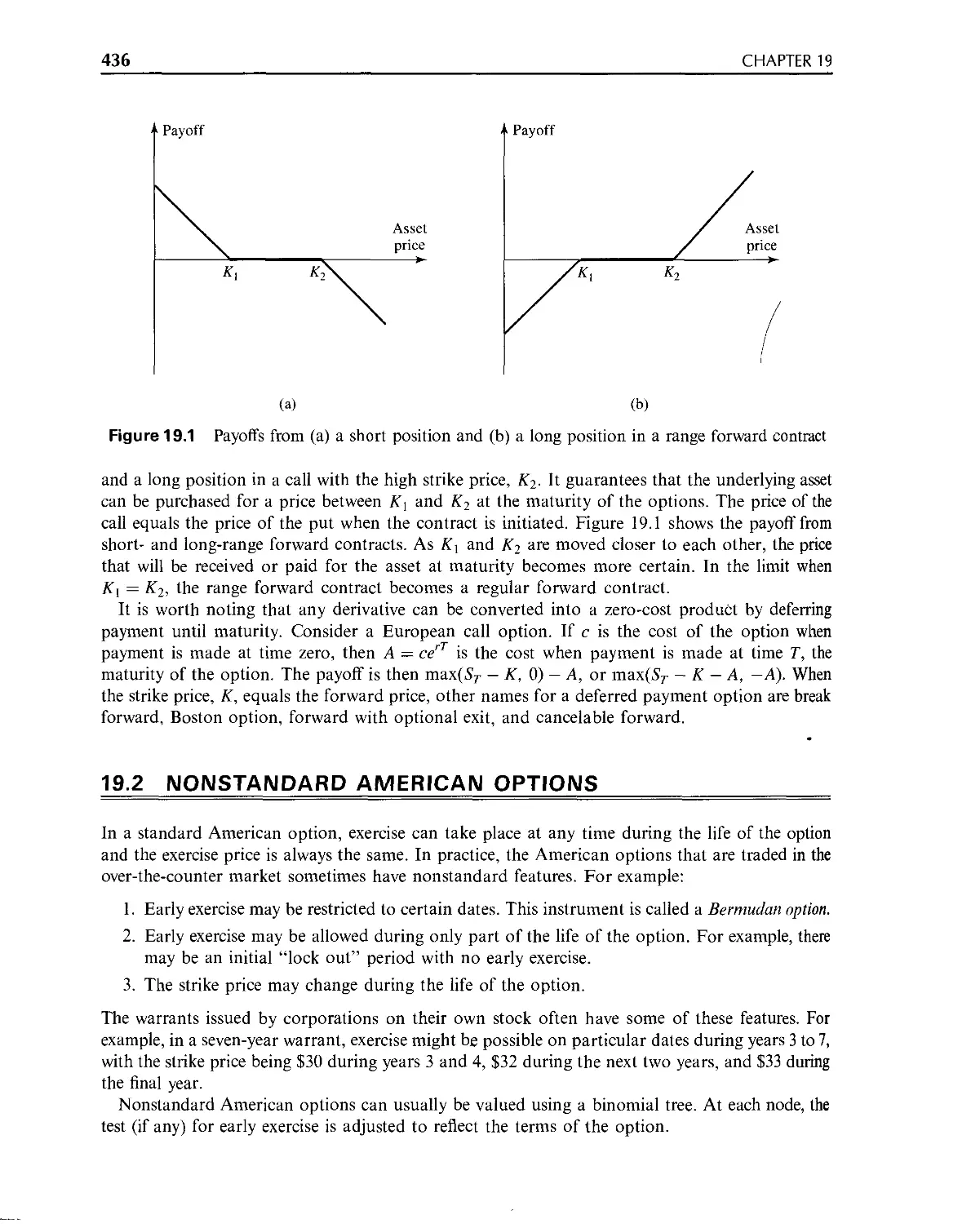

19.1 Packages.....................................................................435

19.2 Nonstandard American options.................................................436

19.3 Forward start options........................................................437

19.4 Compound options.............................................................437

19.5 Chooser options..............................................................438

19.6 Barrier options..............................................................439

19.7 Binary options...............................................................441

19.8 Lookback options.............................................................441

19.9 Shout options................................................................443

19.10 Asian options................................................................443

19.11 Options to exchange one asset for another....................................445

19.12 Basket options...............................................................446

19.13 Hedging issues...............................................................447

19.14 Static options replication...................................................447

Summary.....................................................................449

Suggestions for further reading.............................................449

Questions and problems......................................................451

Assignment questions........................................................452

Appendix 19A: Calculation of the first two moments of arithmetic averages

and baskets.................................................................454

20. More on models and numerical procedures................................................456

20.1 The CEV model................................................................456

20.2 The jump diffusion model.....................................................457

Contents

XV

20.3 Stochastic volatility models.................................................458

20.4 The IVF model................................................................460

20.5 Path-dependent derivatives...................................................461

20.6 Lookback options.............................................................465

20.7 Barrier options..............................................................467

20.8 Options on two correlated assets.............................................472

20.9 Monte Carlo simulation and American options..................................474

Summary.....................................................................478

Suggestions for further reading.............................................479

Questions and problems......................................................480

Assignment questions........................................................481

21. Martingales and measures...............................................................483

21.1 The market price of risk.....................................................484

21.2 Several state variables...................-..................................487

21.3 Martingales..................................................................488

21.4 Alternative choices for the numeraire........................................489

21.5 Extension to multiple independent factors....................................492

21.6 Applications.................................................................493

21.7 Change of numeraire..........................................................495

21.8 Quantos......................................................................497

21.9 Siegel’s paradox.............................................................499

Summary.....................................................................500

Suggestions for further reading.............................................500

Questions and problems......................................................501

Assignment questions........................................................502

Appendix 21 A: Generalizations of Ito’s lemma...............................504

Appendix 2IB: Expected excess return when there are multiple sources of

uncertainty.................................................................506

22. Interest rate derivatives: the standard market models..................................508

22.1 Black’s model................................................................508

22.2 Bond options.................................................................511

22.3 Interest rate caps...........................................................515

22.4 European swap options........................................................520

22.5 Generalizations..............................................................524

22.6 Convexity adjustments........................................................524

22.7 Timing adjustments...........................................................527

22.8 Natural time lags............................................................529

22.9 Hedging interest rate derivatives............................................530

Summary.....................................................................531

Suggestions for further reading.............................................531

Questions and problems......................................................532

Assignment questions........................................................534

Appendix 22A: Proof of the convexity adjustment formula.....................536

23. Interest rate derivatives: models of the short rate....................................537

23.1 Equilibrium models...........................................................537

23.2 One-factor equilibrium models................................................538

23.3 The Rendleman and Bartter model..............................................538

23.4 The Vasicek model............................................................539

23.5 The Cox, Ingersoll, and Ross model...........................................542

23.6 Two-factor equilibrium models................................................543

23.7 No-arbitrage models..........................................................543

23.8 The Ho and Lee model.........................................................544

23.9 The Hull and White model.....................................................546

xvi Contents

23.10 Options on coupon-bearing bonds..............................................549

23.11 Interest rate trees..........................................................550

23.12 A general tree-building procedure............................................552

23.13 Nonstationary models.........................................................563

23.14 Calibration..................................................................564

23.15 Hedging using a one-factor model.............................................565

23.16 Forward rates and futures rates..............................................566

Summary.....................................................................566

Suggestions for further reading.............................................567

Questions and problems......................................................568

Assignment questions........................................................570

24. Interest rate derivatives: more advanced models........................................571

24.1 Two-factor models of the short rate..........................................571

24.2 The Heath, Jarrow, and Morton model..........................................574

24.3 The LIBOR market model.......................................................577

24.4 Mortgage-backed securities................................................. 586

Summary.....................................................................588

Suggestions for further reading.............................................589

Questions and problems......................................................590

Assignment questions........................................................591

Appendix 24A: The A(t, T), nP, and 0(t) functions in the two-factor Hull-White

model........................................................................593

25. Swaps revisited.........................................................................594

25.1 Variations on the vanilla deal...............................................594

25.2 Compounding swaps............................................................595

25.3 Currency swaps...............................................................598

25.4 More complex swaps...........................................................598

25.5 Equity swaps.................................................................601

25.6 Swaps with embedded options..................................................602

25.7 Other swaps..................................................................605

25.8 Bizarre deals................................................................605

Summary.....................................................................606

Suggestions for further reading.............................................606

Questions and problems......................................................607

Assignment questions........................................................607

Appendix 25A: Valuation of an equity swap between payment dates.............609

26. Credit risk.............................................................................610

23.1 Bond prices and the probability of default...................................610

26.2 Historical data..............................................................619

26.3 Bond prices vs. historical default experience................................619

26.4 Risk-neutral vs. real-world estimates........................................620

26.5 Using equity prices to estimate default probabilities........................621

26.6 The loss given default.......................................................623

26.7 Credit ratings migration.....................................................626

26.8 Default correlations.........................................................627

26.9 Credit value at risk.........................................................630

Summary.....................................................................633

Suggestions for further reading.............................................633

Questions and problems......................................................634

Assignment questions........................................................635

Appendix 26A: Manipulation of the matrices of credit rating changes.........636

Contents

xvii

27. Credit derivatives.......................................................................637

27.1 Credit default swaps..........................................................637

27.2 Total return swaps............................................................644

27.3 Credit spread options.........................................................645

27.4 Collateralized debt obligations...............................................646

27.5 Adjusting derivative prices for default risk..................................647

27.6 Convertible bonds.............................................................652

Summary.......................................................................655

Suggestions for further reading...............................................655

Questions and problems........................................................656

Assignment questions..........................................................658

28. Real options.............................................................................660

28.1 Capital investment appraisal..................................................660

28.2 Extension of the risk-neutral valuation framework.............................661

28.3 Estimating the market price of risk...........................................665

28.4 Application to the valuation of a new business................................666

28.5 Commodity prices..............................................................667

28.6 Evaluating options in an investment opportunity...............................670

Summary.......................................................................675

Suggestions for further reading...............................................676

Questions and problems........................................................676

Assignment questions......................................................... 677

29. Insurance, weather, and energy derivatives...............................................678

29.1 Review of pricing issues......................................................678

29.2 Weather derivatives...........................................................679

29.3 Energy derivatives............................................................680

29.4 Insurance derivatives.........................................................682

Summary.......................................................................683

Suggestions for further reading...............................................684

Questions and problems........................................................684

Assignment questions..........................................................685

30. Derivatives mishaps and what we can learn from them......................................686

30.1 Lessons for all users of derivatives..........................................686

30.2 Lessons for financial institutions............................................690

30.3 Lessons for nonfinancial corporations.........................................693

Summary.......................................................................694

Suggestions for further reading...............................................695

Glossary of notation..........................................................................697

Glossary of terms.............................................................................700

DerivaGem software..............................................................:.............715

Major exchanges trading futures and options...................................................720

Table for N(x) when x C 0.....................................................................722

Table for N(x) when x 0.......................................................................723

Author index..................................................................................725

Subject index.................................................................................729

PREFACE

It is sometimes hard for me to believe that the first edition of this book was only 330 pages and

13 chapters long! There have been many developments in derivatives markets over the last 15 years

and the book has grown to keep up with them. The fifth edition has seven new chapters that cover

new derivatives instruments and recent research advances.

Like earlier editions, the book serves several markets. It is appropriate for graduate courses in

business, economics, and financial engineering. It can be used on advanced undergraduate courses

when students have good quantitative skills. Also, many practitioners who want to acquire a

working knowledge of how derivatives can be analyzed find the book useful.

One of the key decisions that must be made by an author who is writing in the area of derivatives

concerns the use of mathematics. If the level of mathematical sophistication is too high, the

material is likely to be inaccessible to many students and practitioners. If it is too low, some

important issues will inevitably be treated in a rather superficial way. I have tried to be particularly

careful about the way I use both mathematics and notation in the book. Nonessential mathema-

tical material has been either eliminated or included in end-of-chapter appendices. Concepts that

are likely to be new to many readers have been explained carefully, and many numerical examples

have been included.

The book covers both derivatives markets and risk management. It assumes that the reader has

taken an introductory course in finance and an introductory course in probability and statistics.

No prior knowledge of options, futures contracts, swaps, and so on is assumed. It is not therefore

necessary for students to take an elective course in investments prior to taking a course based on

this book. There are many different ways the book can be used in the classroom. Instructors

teaching a first course in derivatives may wish to spend most time on the first half of the book.

Instructors teaching a more advanced course will find that many different combinations of the

chapters in the second half of the book can be used. I find that the material in Chapters 29 and 30

works well at the end of either an introductory or an advanced course.

What's New?

Material has been updated and improved throughout the book. The changes in this edition

include:

1. A new chapter on the use of futures for hedging (Chapter 4). Part of this material was

previously in Chapters 2 and 3. The change results in the first three chapters being less

intense and allows hedging to be covered in more depth.

2. A new chapter on models and numerical procedures (Chapter 20). Much of this material is

new, but some has been transferred from the chapter on exotic options in the fourth edition.

xix

XX

Preface

3. A new chapter on swaps (Chapter 25). This gives the reader an appreciation of the range of

nonstandard swap products that are traded in the over-the-counter market and discusses how

they can be valued.

4. There is an extra chapter on credit risk. Chapter 26 discusses the measurement of credit risk

and credit value at risk while Chapter 27 covers credit derivatives.

5. There is a new chapter on real options (Chapter 28).

6. There is a new chapter on insurance, weather, and energy derivatives (Chapter 29).

7. There is a new chapter on derivatives mishaps and what we can learn from them (Chapter 30).

8. The chapter on martingales and measures has been improved so that the material flows

better (Chapter 21).

9. The chapter on value at risk has been rewritten so that it provides a better balance between

the historical simulation approach and the model-building approach (Chapter 16).

10. The chapter on volatility smiles has been improved and appears earlier in the book.

(Chapter 15).

11. The coverage of the LIBOR market model has been expanded (Chapter 24).

12. One or two changes have been made to the notation. The most significant is that the strike

price is now denoted by К rather than X.

13. Many new end-of-chapter problems have been added.

Software

A new version of DerivaGem (Version 1.50) is released with this book. This consists of two Excel

applications: the Options Calculator and the Applications Builder. The Options Calculator consists

of the software in the previous release (with minor improvements). The Applications Builder

consists of a number of Excel functions from which users can build their own applications. It

includes a number of sample applications and enables students to explore the properties of options

and numerical procedures more easily. It also allows more interesting assignments to be designed.

The software is described more fully at the end of the book. Updates to the software can be

downloaded from my website:

www.rotman.utoronto.ca/~hull

Slides

Several hundred PowerPoint slides can be downloaded from my website. Instructors who adopt the

text are welcome to adapt the slides to meet their own needs.

Answers to Questions

As in the fourth edition, end-of-chapter problems are divided into two groups: “Questions and

Problems” and “Assignment Questions”. Solutions to the Questions and Problems are in Options,

Futures, and Other Derivatives: Solutions Manual, which is published by Prentice Hall and can be

purchased by students. Solutions to Assignment Questions are available only in the Instructors

Manual.

Preface

xxi

A ckno wledgmen ts

Many people have played a part in the production of this book. Academics, students, and

practitioners who have made excellent and useful suggestions include Farhang Aslani, Jas Badyal,

Emilio Barone, Giovanni Barone-Adesi, Alex Bergier, George Blazenko, Laurence Booth, Phelim

Boyle, Peter Carr, Don Chance, J.-P. Chateau, Ren-Raw Chen, George Constantinides, Michel

Crouhy, Emanuel Derman, Brian Donaldson, Dieter Dorp, Scott Drabin, Jerome Duncan, Steinar

Ekern, David Fowler, Louis Gagnon, Dajiang Guo, Jrgen Hallbeck, Ian Hawkins, Michael

Hemler, Steve Heston, Bernie Hildebrandt, Michelle Hull, Kiyoshi Kato, Kevin Kneafsy, Tibor

Kucs, Iain MacDonald, Bill Margrabe, Izzy Nelkin, Neil Pearson, Paul Potvin, Shailendra Pandit,

Eric Reiner, Richard Rendleman, Gordon Roberts, Chris Robinson, Cheryl Rosen, John Rumsey,

Ani Sanyal, Klaus Schurger, Eduardo Schwartz, Michael Selby, Piet Sercu, Duane Stock, Edward

Thorpe, Yisong Tian, P. V. Viswanath, George Wang, Jason Wei, Bob Whaley, Alan White,

Hailiang Yang, Victor Zak, and Jozef Zemek. Huafen (Florence) Wu and Matthew Merkley

provided excellent research assistance.

I am particularly grateful to Eduardo Schwartz, who read the original manuscript for the first

edition and made many comments that led to significant improvements, and to Richard Rendle-

man and George Constantinides, who made specific suggestions that led to improvements in more

recent editions.

The first four editions of this book were very popular with practitioners and their comments and

suggestions have led to many improvements in the book. The students in my elective courses on

derivatives at the University of Toronto have also influenced the evolution of the book.

Alan White, a colleague at the University of Toronto, deserves a special acknowledgment. Alan

and I have been carrying out joint research in the area of derivatives for the last 18 years. During

that time we have spent countless hours discussing different issues concerning derivatives. Many of

the new ideas in this book, and many of the new ways used to explain old ideas, are as much Alan’s

as mine. Alan read the original version of this book very carefully and made many excellent

suggestions for improvement. Alan has also done most of the development work on the Deriva-

Gem software.

Special thanks are due to many people at Prentice Hall for their enthusiasm, advice, and

encouragement. I would particularly like to thank Mickey Cox (my editor), P. J. Boardman (the

editor-in-chief) and Kerri Limpert (the production editor). I am also grateful to Scott Barr, Leah

Jewell, Paul Donnelly, and Maureen Riopelle, who at different times have played key roles in the

development of the book.

I welcome comments on the book from readers. My email address is:

hull@rotman.utoronto.ca

John C. Hull

University of Toronto

CHAPTER 1

INTRODUCTION

In the last 20 years derivatives have become increasingly important in the world of finance. Futures

and options are now traded actively on many exchanges throughout the world. Forward contracts,

swaps, and many different types of options are regularly traded outside exchanges by financial

institutions, fund managers, and corporate treasurers in what is termed the over-the-counter

market. Derivatives are also sometimes added to a bond or stock issue.

A derivative can be defined as a financial instrument whose value depends on (or derives from)

the values of other, more basic underlying variables. Very often the variables underlying deriva-

tives are the prices of traded assets. A stock option, for example, is a derivative whose value is

dependent on the price of a stock. However, derivatives can be dependent on almost any variable,

from the price of hogs to the amount of snow falling at a certain ski resort.

Since the first edition of this book was published in 1988, there have been many developments in

derivatives markets. There is now active trading in credit derivatives, electricity derivatives, weather

derivatives, and insurance derivatives. Many new types of interest rate, foreign exchange, and

equity derivative products have been created. There have been many new ideas in risk management

and risk measurement. Analysts have also become more aware of the need to analyze what are

known as real options. (These are the options acquired by a company when it invests in real assets

such as real estate, plant, and equipment.) This edition of the book reflects all these developments.

In this opening chapter we take a first look at forward, futures, and options markets and provide

an overview of how they are used by hedgers, speculators, and arbitrageurs. Later chapters will give

more details and elaborate on many of the points made here.

1.1 EXCHANGE-TRADED MARKETS

A derivatives exchange is a market where individuals trade standardized contracts that have been

defined by the exchange. Derivatives exchanges have existed for a long time. The Chicago Board of

Trade (CBOT, www.cbot.com) was established in 1848 to bring farmers and merchants together.

Initially its main task was to standardize the quantities and qualities of the grains that were traded.

Within a few years the first futures-type contract was developed. It was known as a to-arrive

contract. Speculators soon became interested in the contract and found trading the contract to be

an attractive alternative to trading the grain itself. A rival futures exchange, the Chicago

Mercantile Exchange (CME, www.cme.com), was established in 1919. Now futures exchanges

exist all over the world.

The Chicago Board Options Exchange (СВОЕ, www.cboe.com) started trading call option

1

2

CHAPTER 1

contracts on 16 stocks in 1973. Options had traded prior to 1973 but the СВОЕ succeeded in

creating an orderly market with well-defined contracts. Put option contracts started trading on the

exchange in 1977. The СВОЕ now trades options on over 1200 stocks and many different stock

indices. Like futures, options have proved to be very popular contracts. Many other exchanges

throughout the world now trade options. The underlying assets include foreign currencies and

futures contracts as well as stocks and stock indices.

Traditionally derivatives traders have met on the floor of an exchange and used shouting and a

complicated set of hand signals to indicate the trades they would like to carry out. This is known as

the open outcry system. In recent years exchanges have increasingly moved from the open outcry

system to electronic trading. The latter involves traders entering their desired trades at a keyboard

and a computer being used to match buyers and sellers. There seems little doubt that eventually all

exchanges will use electronic trading.

1.2 OVER-THE-COUNTER MARKETS

Not all trading is done on exchanges. The over-the-counter market is an important alternative to

exchanges and, measured in terms of the total volume of trading, has become much larger than the

exchange-traded market. It is a telephone- and computer-linked network of dealers, who do not

physically meet. Trades are done over the phone and are usually between two financial institutions

or between a financial institution and one of its corporate clients. Financial institutions often act as

market makers for the more commonly traded instruments. This means that they are always

prepared to quote both a bid price (a price at which they are prepared to buy) and an offer price

(a price at which they are prepared to sell).

Telephone conversations in the over-the-counter market are usually taped. If there is a dispute

about what was agreed, the tapes are replayed to resolve the issue. Trades in the over-the-counter

market are typically much larger than trades in the exchange-traded market. A key advantage of

the over-the-counter market is that the terms of a contract do not have to be those specified by an

exchange. Market participants are free to negotiate any mutually attractive deal. A disadvantage is

that there is usually some credit risk in an over-the-counter trade (i.e., there is a small risk that the

contract will not be honored). As mentioned earlier, exchanges have organized themselves to

eliminate virtually all credit risk.

1.3 FORWARD CONTRACTS

A forward contract is a particularly simple derivative. It is an agreement to buy or sell an asset at a

certain future time for a certain price. It can be contrasted with a spot contract, which is an

agreement to buy or sell an asset today. A forward contract is traded in the over-the-counter

market—usually between two financial institutions or between a financial institution and one of its

clients.

One of the parties to a forward contract assumes a long position and agrees to buy the underlying

asset on a certain specified future date for a certain specified price. The other party assumes a short

position and agrees to sell the asset on the same date for the same price.

Forward contracts on foreign exchange are very popular. Most large banks have a “forward

desk” within their foreign exchange trading room that is devoted to the trading of forward

Introduction

3

Table 1.1 Spot and forward quotes for the USD-GBP exchange

rate, August 16, 2001 (GBP = British pound; USD = U.S. dollar)

Bid Offer

Spot 1.4452 1.4456

1-month forward 1.4435 1.4440

3-month forward 1.4402 1.4407

6-month forward 1.4353 1.4359

1-year forward 1.4262 1.4268

contracts. Table 1.1 provides the quotes on the exchange rate between the British pound (GBP) and

the U.S. dollar (USD) that might be made by a large international bank on August 16, 2001. The

quote is for the number of USD per GBP. The first quote indicates that the bank is prepared to buy

GBP (i.e., sterling) in the spot market (i.e., for virtually immediate delivery) at the rate of $1.4452

per GBP and sell sterling in the spot market at $ 1.4456 per GBP. The second quote indicates that

the bank is prepared to buy sterling in one month at $1.4435 per GBP and sell sterling in one month

at $1.4440 per GBP; the third quote indicates that it is prepared to buy sterling in three months at

$1.4402 per GBP and sell sterling in three months at $1.4407 per GBP; and so on. These quotes are

for very large transactions. (As anyone who has traveled abroad knows, retail customers face much

larger spreads between bid and offer quotes than those in given Table 1.1.)

Forward contracts can be used to hedge foreign currency risk. Suppose that on August 16, 2001,

the treasurer of a U.S. corporation knows that the corporation will pay £1 million in six months (on

February 16, 2002) and wants to hedge against exchange rate moves. Using the quotes in Table 1.1,

the treasurer can agree to buy £1 million six months forward at an exchange rate of 1.4359. The

corporation then has a long forward contract on GBP. It has agreed that on February 16, 2002, it

will buy £1 million from the bank for $1.4359 million. The bank has a short forward contract on

GBP. It has agreed that on February 16, 2002, it will sell £1 million for $1.4359 million. Both sides

have made a binding commitment.

Payoffs from Forward Contracts

Consider the position of the corporation in the trade we have just described. What are the possible

outcomes? The forward contract obligates the corporation to buy £1 million for $1,435,900. If the

spot exchange rate rose to, say, 1.5000, at the end of the six months the forward contract would be

worth $64,100 (= $1,500,000 — $1,435,900) to the corporation. It would enable £1 million to be

purchased at 1.4359 rather than 1.5000. Similarly, if the spot exchange rate fell to 1.4000 at the end of

the six months, the forward contract would have a negative value to the corporation of $35,900

because it would lead to the corporation paying $35,900 more than the market price for the sterling.

In general, the payoff from a long position in a forward contract on one unit of an asset is

ST - К

where К is the delivery price and ST is the spot price of the asset at maturity of the contract. This is

because the holder of the contract is obligated to buy an asset worth ST for K. Similarly, the payoff

from a short position in a forward contract on one unit of an asset is

K— ST

4

CHAPTER 1

Figure 1.1 Payoffs from forward contracts: (a) long position, (b) short position.

Delivery price = K\ price of asset at maturity = St

These payoffs can be positive or negative. They are illustrated in Figure 1.1. Because it costs

nothing to enter into a forward contract, the payoff from the contract is also the trader’s total gain

or loss from the contract.

Forward Price and Delivery Price

It is important to distinguish between the forward price and delivery price. The forward price is the

market price that would be agreed to today for delivery of the asset at a specified maturity date.

The forward price is usually different from the spot price and varies with the maturity date

(see Table 1.1).

In the example we considered earlier, the forward price on August 16, 2001, is 1.4359 for a

contract maturing on February 16, 2002. The corporation enters into a contract and 1.4359

becomes the delivery price for the contract. As we move through time the delivery price for the

corporation’s contract does not change, but the forward price for a contract maturing on February

16, 2002, is likely to do so. For example, if GBP strengthens relative to USD in the second half of

August the forward price could rise to 1.4500 by September 1, 2001.

Forward Prices and Spot Prices

We will be discussing in some detail the relationship between spot and forward prices in Chapter 3.

In this section we illustrate the reason why the two are related by considering forward contracts on

gold. We assume that there are no storage costs associated with gold and that gold earns no income.1

Suppose that the spot price of gold is $300 per ounce and the risk-free interest rate for

investments lasting one year is 5% per annum. What is a reasonable value for the one-year

forward price of gold?

1 This is not totally realistic. In practice, storage costs are close to zero, but an income of 1 to 2% per annum can be

earned by lending gold.

Introduction

5

Suppose first that the one-year forward price is $340 per ounce. A trader can immediately take

the following actions:

1. Borrow $300 at 5% for one year.

2. Buy one ounce of gold.

3. Enter into a short forward contract to sell the gold for $340 in one year.

The interest on the $300 that is borrowed (assuming annual compounding) is $15. The trader can,

therefore, use $315 of the $340 that is obtained for the gold in one year to repay the loan. The

remaining $25 is profit. Any one-year forward price greater than $315 will lead to this arbitrage

trading strategy being profitable.

Suppose next that the forward price is $300. An investor who has a portfolio that includes gold can

1. Sell the gold for $300 per ounce.

2. Invest the proceeds at 5%.

3. Enter into a long forward contract to repurchase the gold in one year for $300 per ounce.

When this strategy is compared with the alternative strategy of keeping the gold in the portfolio for

one year, we see that the investor is better off by $15 per ounce. In any situation where the forward

price is less than $315, investors holding gold have an incentive to sell the gold and enter into a

long forward contract in the way that has been described.

The first strategy is profitable when the one-year forward price of gold is greater than $315. As

more traders attempt to take advantage of this strategy, the demand for short forward contracts

will increase and the one-year forward price of gold will fall. The second strategy is profitable for

all investors who hold gold in their portfolios when the one-year forward price of gold is less than

$315. As these investors attempt to take advantage of this strategy, the demand for long forward

contracts will increase and the one-year forward price of gold will rise. Assuming that individuals

are always willing to take advantage of arbitrage opportunities when they arise, we can conclude

that the activities of traders should cause the one-year forward price of gold to be exactly $315.

Any other price leads to an arbitrage opportunity.2

1.4 FUTURES CONTRACTS

Like a forward contract, a futures contract is an agreement between two parties to buy or sell an

asset at a certain time in the future for a certain price. Unlike forward contracts, futures contracts

are normally traded on an exchange. To make trading possible, the exchange specifies certain

standardized features of the contract. As the two parties to the contract do not necessarily know

each other, the exchange also provides a mechanism that gives the two parties a guarantee that the

contract will be honored.

The largest exchanges on which futures contracts are traded are the Chicago Board of Trade

(CBOT) and the Chicago Mercantile Exchange (CME). On these and other exchanges throughout

the world, a very wide range of commodities and financial assets form the underlying assets in the

various contracts. The commodities include pork bellies, live cattle, sugar, wool, lumber, copper,

aluminum, gold, and tin. The financial assets include stock indices, currencies, and Treasury bonds.

2 Our arguments make the simplifying assumption that the rate of interest on borrowed funds is the same as the rate

of interest on invested funds.

6

CHAPTER 1

One way in which a futures contract is different from a forward contract is that an exact delivery

date is usually not specified. The contract is referred to by its delivery month, and the exchange

specifies the period during the month when delivery must be made. For commodities, the delivery

period is often the entire month. The holder of the short position has the right to choose the time

during the delivery period when it will make delivery. Usually, contracts with several different

delivery months are traded at any one time. The exchange specifies the amount of the asset to be

delivered for one contract and how the futures price is to be quoted. In the case of a commodity,

the exchange also specifies the product quality and the delivery location. Consider, for example, the

wheat futures contract currently traded on the Chicago Board of Trade. The size of the contract is

5,000 bushels. Contracts for five delivery months (March, May, July, September, and December)

are available for up to 18 months into the future. The exchange specifies the grades of wheat that

can be delivered and the places where delivery can be made.

Futures prices are regularly reported in the financial press. Suppose that on September 1, the

December futures price of gold is quoted as $300. This is the price, exclusive of commissions, at

which traders can agree to buy or sell gold for December delivery. It is determined on the floor of the

exchange in the same way as other prices (i.e., by the laws of supply and demand). If more traders

want to go long than to go short, the price goes up; if the reverse is true, the price goes down.3

Further details on issues such as margin requirements, daily settlement procedures, delivery

procedures, bid-offer spreads, and the role of the exchange clearinghouse are given in Chapter 2.

1.5 OPTIONS

Options are traded both on exchanges and in the over-the-counter market. There are two basic

types of options. A call option gives the holder the right to buy the underlying asset by a certain date

for a certain price. A put option gives the holder the right to sell the underlying asset by a certain

date for a certain price. The price in the contract is known as the exercise price or strike price-, the

date in the contract is known as the expiration date or maturity. American options can be exercised at

any time up to the expiration date. European options can be exercised only on the expiration date

itself.4 Most of the options that are traded on exchanges are American. In the exchange-traded

equity options market, one contract is usually an agreement to buy or sell 100 shares. European

options are generally easier to analyze than American options, and some of the properties of an

American option are frequently deduced from those of its European counterpart.

It should be emphasized that an option gives the holder the right to do something. The holder

does not have to exercise this right. This is what distinguishes options from forwards and futures,

where the holder is obligated to buy or sell the underlying asset. Note that whereas it costs nothing

to enter into a forward or futures contract, there is a cost to acquiring an option.

Call Options

Consider the situation of an investor who buys a European call option with a strike price of $60 to

purchase 100 Microsoft shares. Suppose that the current stock price is $58, the expiration date of

3 In Chapter 3 we discuss the relationship between a futures price and the spot price of the underlying asset (gold, in

this case).

4 Note that the terms American and European do not refer to the location of the option or the exchange. Some

options trading on North American exchanges are European.

Introduction

7

Figure 1.2 Profit from buying a European call option on one Microsoft share.

Option price = $5; strike price = $60

the option is in four months, and the price of an option to purchase one share is $5. The initial

investment is $500. Because the option is European, the investor can exercise only on the expiration

date. If the stock price on this date is less than $60, the investor will clearly choose not to exercise.

(There is no point in buying, for $60, a share that has a market value of less than $60.) In these

circumstances, the investor loses the whole of the initial investment of $500. If the stock price is

above $60 on the expiration date, the option will be exercised. Suppose, for example, that the stock

price is $75. By exercising the option, the investor is able to buy 100 shares for $60 per share. If the

shares are sold immediately, the investor makes a gain of $15 per share, or $1,500, ignoring

transactions costs. When the initial cost of the option is taken into account, the net profit to the

investor is $1,000.

Figure 1.2 shows how the investor’s net profit or loss on an option to purchase one share varies

with the final stock price in the example. (We ignore the time value of money in calculating the

profit.) It is important to realize that an investor sometimes exercises an option and makes a loss

overall. Suppose that in the example Microsoft’s stock price is $62 at the expiration of the option.

The investor would exercise the option for a gain of 100 x ($62 — $60) = $200 and realize a loss

overall of $300 when the initial cost of the option is taken into account. It is tempting to argue that

the investor should not exercise the option in these circumstances. However, not exercising would

lead to an overall loss of $500, which is worse than the $300 loss when the investor exercises. In

general, call options should always be exercised at the expiration date if the stock price is above the

strike price.

Put Options

Whereas the purchaser of a call option is hoping that the stock price will increase, the purchaser of a

put option is hoping that it will decrease. Consider an investor who buys a European put option to

sell 100 shares in IBM with a strike price of $90. Suppose that the current stock price is $85, the

expiration date of the option is in three months, and the price of an option to sell one share is $7. The

initial investment is $700. Because the option is European, it will be exercised only if the stock price

is below $90 at the expiration date. Suppose that the stock price is $75 on this date. The investor can

8

CHAPTER 1

Figure 1.3 Profit from buying a European put option on one IBM share.

Option price = $7; strike price = $90

buy 100 shares for $75 per share and, under the terms of the put option, sell the same shares for $90

to realize a gain of $15 per share, or $1,500 (again transactions costs are ignored). When the $700

initial cost of the option is taken into account, the investor’s net profit is $800. There is no guarantee

that the investor will make a gain. If the final stock price is above $90, the put option expires

worthless, and the investor loses $700. Figure 1.3 shows the way in which the investor’s profit or loss

on an option to sell one share varies with the terminal stock price in this example.

Early Exercise

As already mentioned, exchange-traded stock options are usually American rather than European.

That is, the investor in the foregoing examples would not have to wait until the expiration date before

exercising the option. We will see in later chapters that there are some circumstances under which it is

optimal to exercise American options prior to maturity.

Option Positions

There are two sides to every option contract. On one side is the investor who has taken the long

position (i.e., has bought the option). On the other side is the investor who has taken a short

position (i.e., has sold or written the option). The writer of an option receives cash up front, but

has potential liabilities later. The writer’s profit or loss is the reverse of that for the purchaser of the

option. Figures 1.4 and 1.5 show the variation of the profit or loss with the final stock price for

writers of the options considered in Figures 1.2 and 1.3.

There are four types of option positions:

1. A long position in a call option.

2. A long position in a put option.

3. A short position in a call option.

4. A short position in a put option.

Introduction

9

Figure 1.4 Profit from writing a European call option on one Microsoft share.

Option price = $5; strike price = $60

It is often useful to characterize European option positions in terms of the terminal value or payoff

to the investor at maturity. The initial cost of the option is then not included in the calculation. If

К is the strike price and ST is the final price of the underlying asset, the payoff from a long position

in a European call option is

max(S7 — K, 0)

This reflects the fact that the option will be exercised if ST > К and will not be exercised if ST < K.

The payoff to the holder of a short position in the European call option is

— max(5r — K, 0) = min(X — ST, 0)

Figure 1.5 Profit from writing a European put option on one IBM share.

Option price = $7; strike price = $90

10

CHAPTER 1

Figure 1.6 Payoffs from positions in European options: (a) long call, (b) short call, (c) long put,

(d) short put. Strike price = K: price of asset at maturity = ST

The payoff to the holder of a long position in a European put option is